Media Contacts

Catherine Theroux

Director, Public Relations

Work Phone: (860) 285-7787

Mobile Phone: (703) 447-3257

Brooke Lacey

Senior Public Relations Specialist

Work Phone: (860) 298-3920

Mobile Phone: (413) 530-6184

12/7/2023

LIMRA forecasts annuity products offering investment protection will continue to drive sales growth

Favorable economic conditions, demographic shifts, and greater consumer demand for lifetime retirement income and investment protection have propelled annuity sales growth over the past two years. In 2022, annuity sales totaled a record high $313 billion. At the end of 2023, LIMRA is projecting sales to exceed $350 billion, largely based on strong fixed annuity sales.

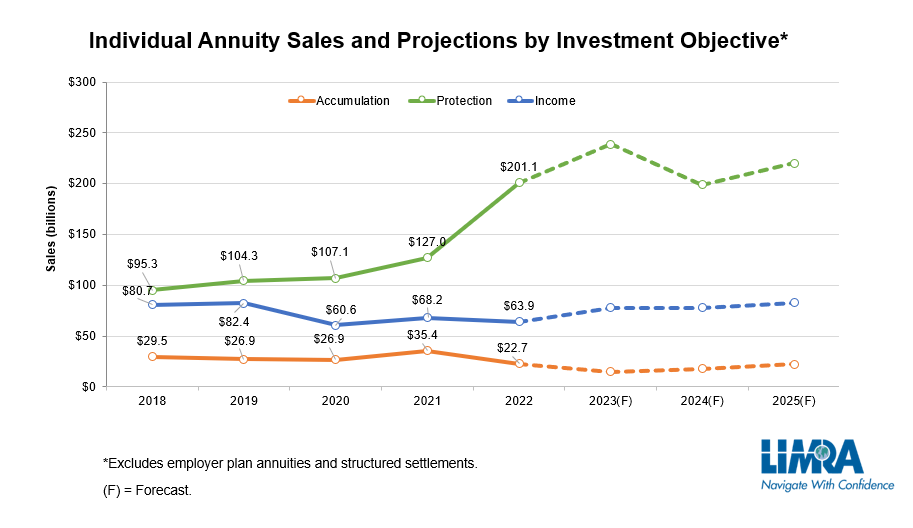

The two years of record annuity sales were fueled by the enormous growth in the fixed annuity market. This growth was driven by rising interest rates, which more than tripled over the past 18 months and allowed carriers to raise their crediting rates. At the same time, market volatility prompted growing demand for products that offer investment protection. LIMRA forecasts that demand for protection products will continue over the next few years.

What’s Ahead in 2024 and 2025

While interest rates are expected to peak in 2023, the forecast for the 10-year Treasury rate is to remain around 4% through 2026. This slight decline will dampen sales growth in 2024, particularly for income annuity products and fixed-rate deferred products. Countering this is the turnaround in the equity markets and the expectation is annuity sales will rebound in 2025.

Overall, LIMRA is forecasting annuity sales to total between $311 billion and $331 billion in 2024. Much of the variance depends on how interest rates play out. As interest rates recover in 2025, sales of indexed annuities and income annuities are expected to return to or exceed the levels set in 2023, with total sales growing as much as 10% and ranging from $342 billion to $362 billion.

Individual Product Line Forecasts

Fixed-rate deferred annuities (FRD) will face growing competition from bank CDs and cash equivalent solutions as short duration rates improve. While FRD sales will be considerably lower (down as much as 30%) than the record high sales set in 2023, FRD sales will likely exceed $100 billion in 2024 and 2025.

Fixed indexed annuities (FIA) will be hampered by the pullback in interest rates, and as crediting rates decline, the demand for protection-based solutions will slow in 2024 and 2025. Despite the expected nominal decline of FIA sales in 2024, sales of this product will remain historically strong and are forecast to reach nearly $100 billion in 2025.

Income annuity sales, although dampened in 2024 by declining interest rates, will benefit from the more than 3 million Americans reaching the typical age range when single premium immediate annuities are purchased over the next two years. LIMRA is predicting income annuity sales to top $15 billion in 2024 and set a new record in 2025 — above $18 billion.

Registered index-linked annuities (RILA) will also have a strong year as steady equity market growth and lower interest rates make the value proposition of RILAs particularly attractive. In 2024 and 2025, LIMRA is forecasting RILA products to expand on the five consecutive years of record sales. RILA sales are likely to be as high as $52 billion in 2024 and $57 billion in 2025.

Traditional variable annuity sales (traditional VA) should benefit from a growing equity market over the next two years, but regulatory headwinds may counter the sales growth potential. LIMRA predicts traditional VA sales to grow as much as 10% to $60 billion in 2024 and increase as much as 8% to $65 billion in 2025.

Director, Public Relations

Work Phone: (860) 285-7787

Mobile Phone: (703) 447-3257

Senior Public Relations Specialist

Work Phone: (860) 298-3920

Mobile Phone: (413) 530-6184